Holistic tax planning and optimisation

Your control is our priority.

Introduction

Our proprietary framework involves managing your wealth in the most tax-efficient manner, relentlessly focusing on helping to protect your wealth from erosion by taxes and aiming to maximise post-tax investment returns.

- Tax-deductible strategies

- Tax-advantaged strategies

- Asset sale tax planning strategies

- Cash flow distribution strategies

- Tax implications for estate planning

- Coordination with tax professionals

- Utilise all of your family’s available tax allowances, every year where possible

- Arrange your assets in the most tax-efficient manner utilising tax-advantaged investments where appropriate

- Holding dividend and interest-paying investments in tax-deferred or tax-efficient accounts

- Tax-smart wealth distribution strategies, with tax-efficient retirement income withdrawal and estate planning

Every investor is looking for an edge that helps them boost their overall wealth. But one strategy that most investors don’t pay enough attention to is tax efficient investing. The reason? Even small reductions in tax costs could potentially have enormous consequences for wealth accumulation when compounded over a number of years.

Your goals and personal philosophy towards taxes are unique and may change over time. For many families, income tax planning and estate planning are key components in their financial plan.

Our recommendations are outcome-based, not tax-driven. We allow your goals and values to determine the best tax strategy. Our clients rely on us for comprehensive solutions that take into account annual income and capital gains taxes, inheritance and estate taxes now and in the future. You are advised to seek independent tax advice from suitably qualified professionals before making any decision as to the tax implications of any investment.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation and reliefs from taxation can change at any time. The value of any tax relief depends on individual circumstances.

Need a bespoke financial plan crafted specifically for your unique requirements?

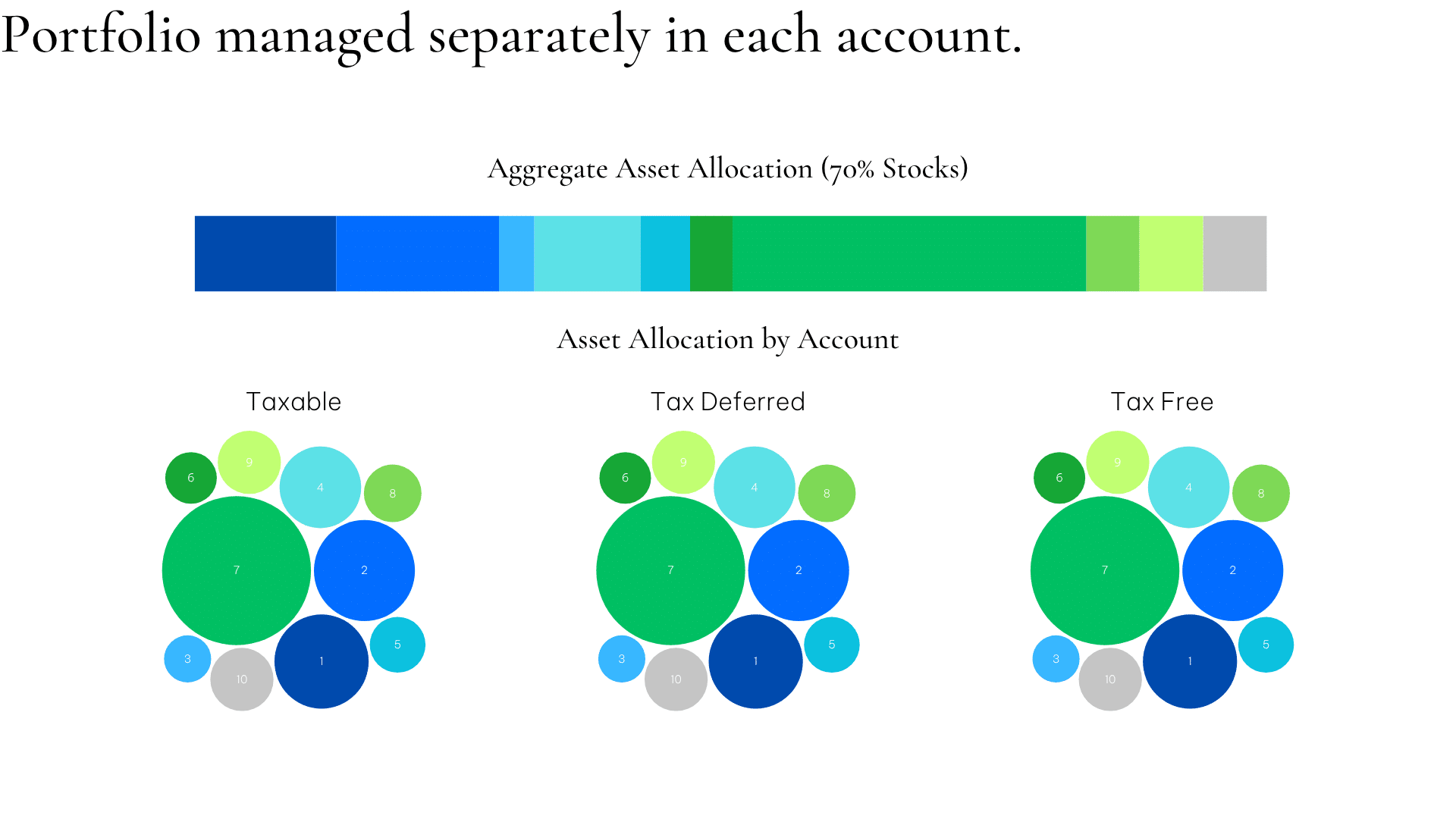

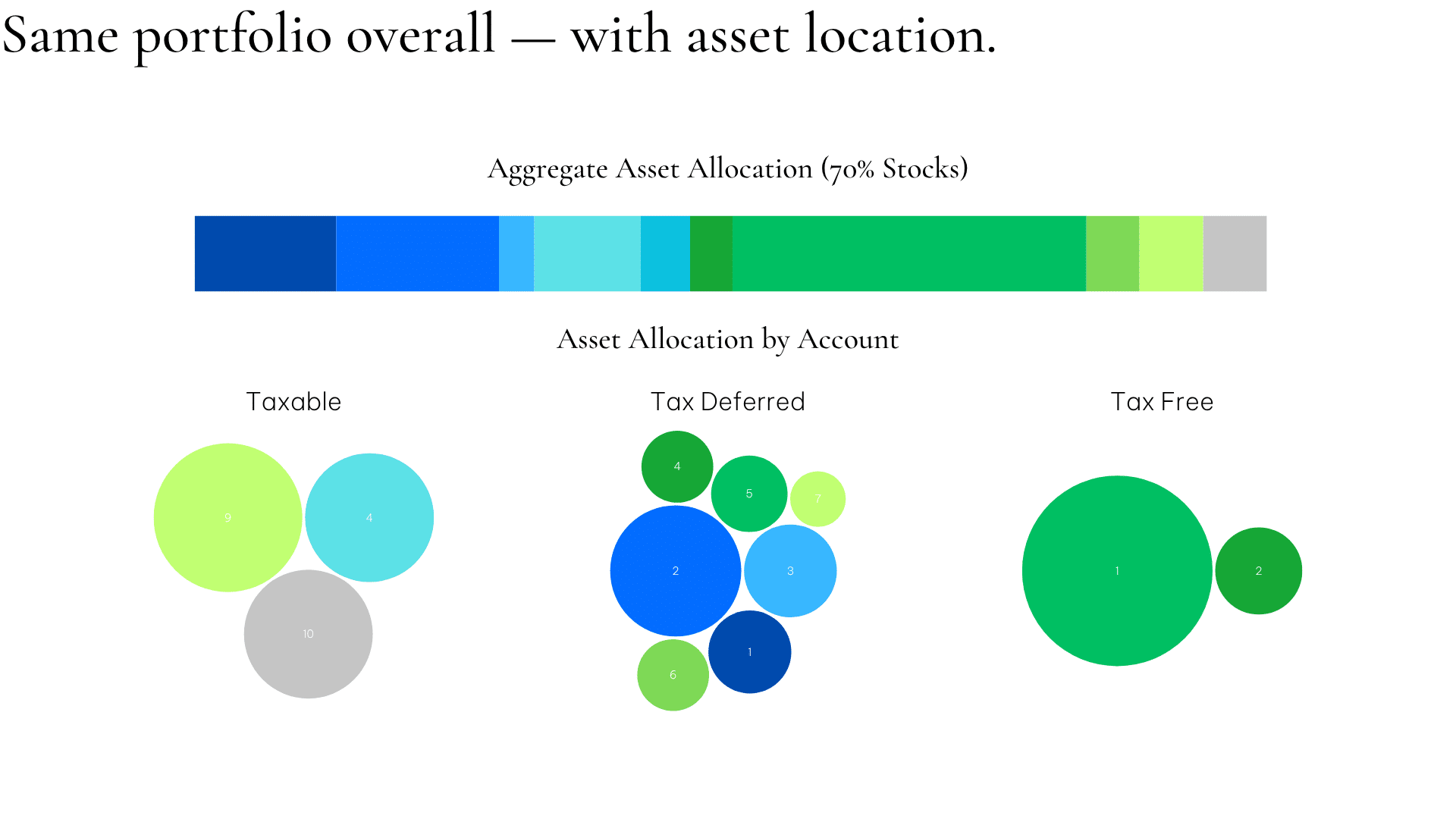

Book a DemoOptimal asset allocation plays a major role in maximising returns, but many investors overlook asset location – a systematic method for enhancing returns without switching out investments.

This strategy involves placing different types of assets in the most tax-efficient wrappers and investments based on their expected tax impact. The goal? Minimising tax drag and maximising after-tax returns.

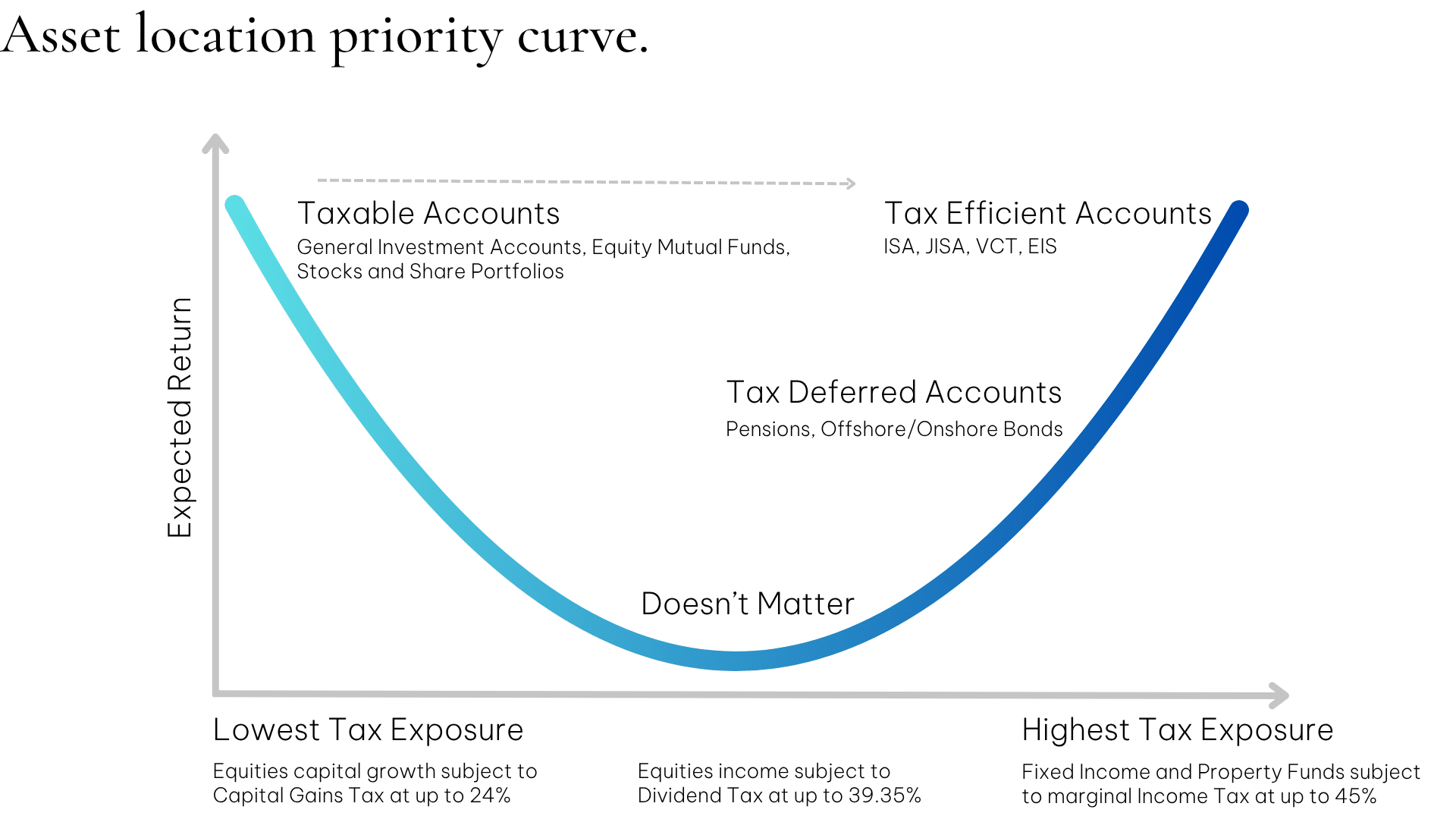

| Asset class | Tax treatment | Taxable accounts | Tax deferred accounts | Tax exempt accounts |

|---|---|---|---|---|

| (Unwrapped unit trusts, OEICS, stocks and shares, portfolios and general investment accounts, private investments) | (Pensions, offshore bonds, onshore bonds) | (ISA, Junior ISAs, VCTs, EIS) | ||

| Equities – capital growth | Capital gains tax Lower rate 18% Upper rate 24% | Neutral | Optimal | Most optimal |

| Equities – dividend income | Dividend tax Basic rate 8.75% Higher rate 33.75% Additional rate 39.35% | Least optimal | More optimal | Most optimal |

| Fixed income & property funds | Marginal income tax Basic rate 20% Higher rate 40% Additional rate 45% | Least optimal | More optimal | Most optimal |

Don’t invest unless you are prepared to lose all the money that you invest. EIS and VCTs are high-risk investments. You may not be able to access your money easily. The legislation and as a result, the tax treatment will depend on individual circumstances, may change in the future, and could apply retrospectively.

Understanding and keeping up-to-date with UK tax regulations can be complex and time consuming. We help our clients by structuring their finances tax efficiently.

With access to a dedicated Tax and Technical team and the Technical Connection division at

St. James’s Place, we are well equipped to devise intelligent tax-efficient investment programmes and help ensure these remain relevant with changing legislation.

As a wealth management firm, we carefully consider the tax implications of dividends, income, and capital gains for each client’s portfolio. The tax planning strategies we use include:

- Matching tax-generating assets with tax-efficient investments

- Offsetting gains with losses whenever appropriate

- Using tax-exempt and tax-advantaged investments as warranted

- Closely monitoring the after-tax return on your investments and reporting taxable distributions to your accountant

Other wealth managers and private banks may report only your investment returns, but they might not be factoring in a key element that could lower what you take home: taxes.

We believe in using noncontentious tax planning to help you maximise the return on your capital and minimise the impact of all the taxes on your wealth. We work with your professional advisers to help ensure your accountant, personal tax adviser, and solicitor are all working together to develop a long-term plan that is tax efficient.

There are many legitimate tax planning opportunities that are available, which we will advise you on and suggest suitable plans that meet your long-term objectives – this is where our skills really make a difference to you and your family.

Our tax-smart retirement income strategy is another way in which different components can complement one another by sequencing withdrawals in a tax-efficient way.

A simple withdrawal sequence might involve withdrawing from taxable accounts first and tax-advantaged accounts last, but even more complex withdrawal sequencing strategies can have a significantly greater impact on lifetime spending power. For example, distributing savings that don’t register as taxable income, like tax-deferred withdrawals from an offshore or onshore bond, and distributions from tax-efficient vehicles such as ISAs.

Overall, how these different approaches are combined can make a significant difference when it comes to building wealth over the long term. Each of them can be helpful in and of themselves, but in concert, they can provide much more significant compounded benefits that can really move the needle. We help you by maximising the use of government allowances, so you can have the lifestyle you deserve;

– Taking a tax-efficient retirement income

– Helping to reduce your Inheritance Tax Bill (IHT)

The value of an investment with St. James’s Place will be directly linked to the performance of the funds selected, and may fall as well as rise. You may get back less than the amount invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time and are generally dependent on individual circumstances.