Introduction

There are now 526,611 pupils attending 1,455 independent schools. On a like-for-like basis, pupil numbers have fallen by 3.8%. Boarding numbers have fallen more sharply still, while the number of new pupils joining independent schools has also reduced. These figures reflect a sector operating in a markedly different environment from that of recent years. Schools continue to adapt to a range of financial, demographic and policy pressures, including the ongoing effects of the introduction of VAT on school fees.1

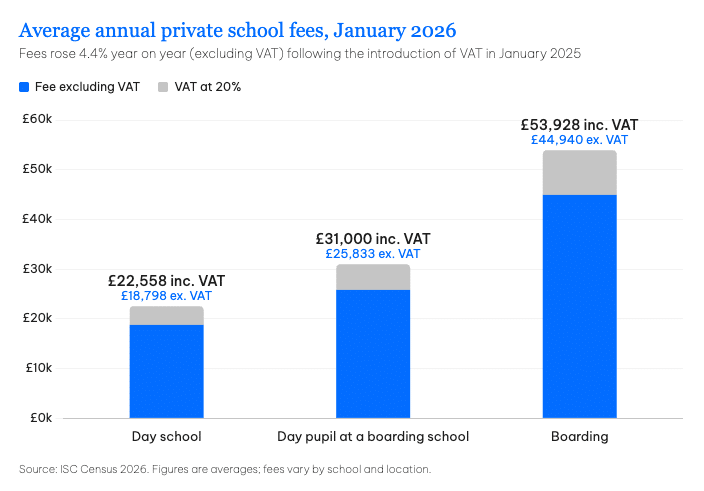

Following the introduction of VAT on independent school fees from January 2025, schools have adopted a range of approaches to fee setting. Across schools completing the Census in both years, average fees increased by 4.4% between January 2025 and January 2026 (excluding VAT).2

The average fee level increases as pupils progress through the different phases of education. In day schools, fees rise by 12.6% between junior and senior phases and by a further 4.0% between senior and sixth form, indicating a steady increase as pupils move through the system.3

While the cost of tuition fees can vary widely depending on the school and location, sending your child to a private school costs, on average, £18,798 per year for attending a day school, or £25,833 per year where a day pupil attends a boarding school, rising to £44,940 for pupils who board.4 These amounts exclude VAT at an additional 20%.

1, 2, 3, 4 ISC Census and Annual Report, June 2026

At a glance

- Parents could face around £400,000-£550,000 in day pupil fees or £950,000 in boarding fees for each child, assuming 14 years at private school and 3.5% per year fee increase.

- ISAs and Investment Bonds can be used as tax wrappers to save towards school fees, potentially making tax-efficient or tax-deferred returns on your investment.

- Unit Trusts and General Investment Accounts (GIAs) may also provide access to investing in various asset classes, with tax treatment dependent on individual circumstances.

Average boarding school fees could cost nearly £1m per child

Taking a tax-efficient approach to saving towards private school fees…

Let’s assume that school fees increase by 3.5% a year. This would be the lowest increase seen over the course of a 14-year education. Based on the average costs, parents could face around £400,000-£550,000 in day pupil fees or £950,000 in boarding fees for each child.

However, while these figures are considerable, the sooner you start saving towards your child’s school fees, the better.

By starting early, saving regularly, and investing, parents could build up a substantial sum over time to help cover the costs of private education.

Taking a tax-efficient approach to school fees can help make private education much more accessible.

Key tax-efficient solutions

An ISA is a tax-efficient investment vehicle that enables parents to put aside a certain amount each year, without incurring any income or capital gains tax (CGT) on the interest or investment returns earned on the savings.

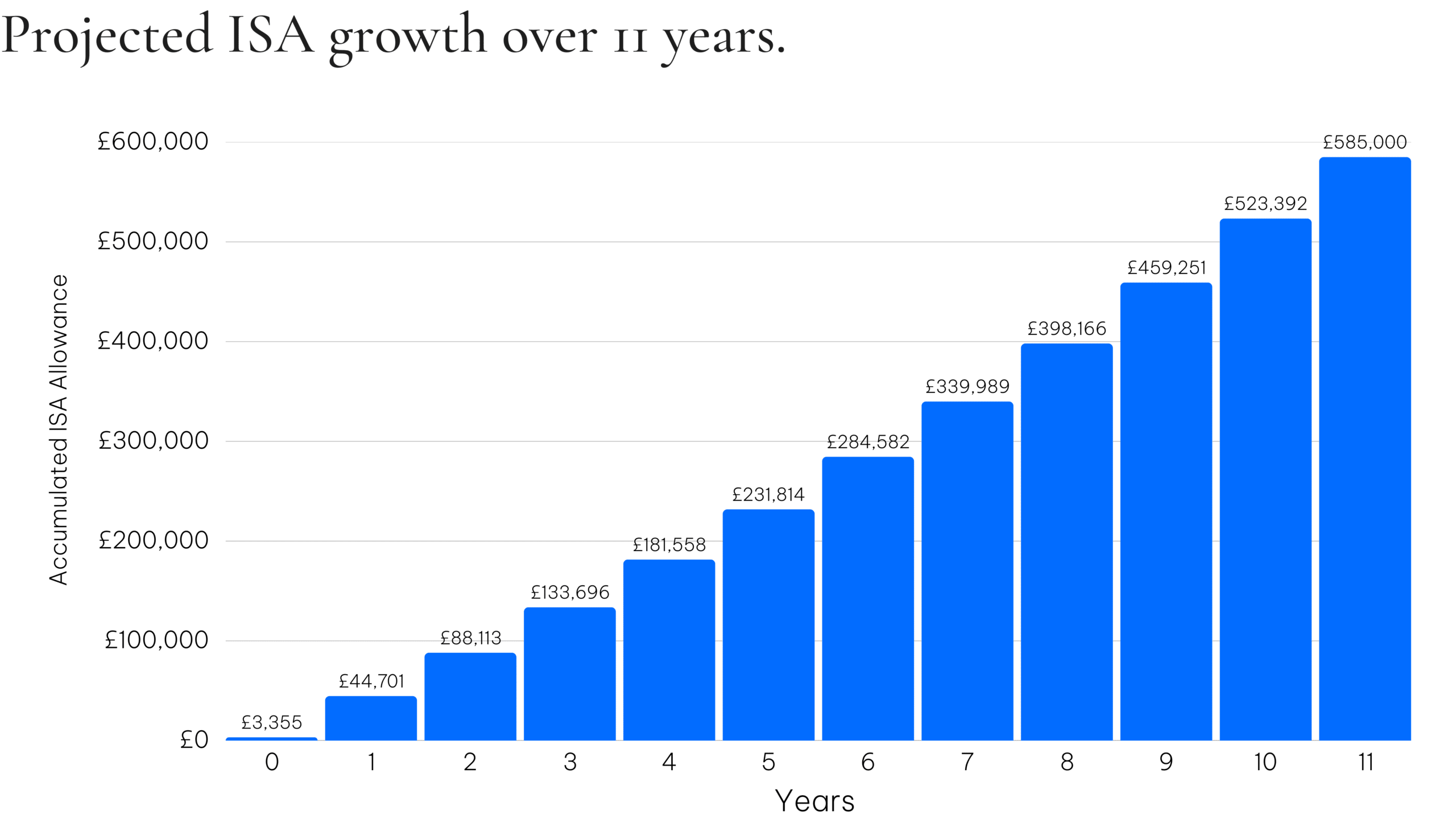

If both parents make monthly contributions that fully utilise their ISA allowance (£20,000 per person in the 2026/27 tax year) from the child’s birth, this could accumulate to a sum of £585,000 by the time the child is 11 years old, based on 5% net annual growth after fees, compounding monthly.* Withdrawals from an ISA are tax efficient, so parents can extract funds as needed to pay for school fees without incurring any capital gains or income tax liability, or invest in other options, such as stocks and shares.

*These figures are examples only and they are not guaranteed – they are not minimum or maximum amounts. What you get back depends on how your investment grows and the tax treatment of the investment.

The value of an ISA with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

The favourable tax treatment of ISAs may be subject to changes in legislation in the future.

An Investment Bond is a tax-efficient investment wrapper that allows parents to save and invest to pay for private school fees. An Investment Bond invests in a range of assets, such as stocks, shares, bonds, and funds. You can invest a lump sum or make regular contributions.

During the term of the investment, returns earned within the bond are not subject to income or capital gains tax (CGT), providing significant tax savings over the long term with the option to draw down up to 5% of your original investment per year on a tax-deferred basis. As the 5% allowance is cumulative, any unused allowance is carried forward for up to 20 years.**

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

**Please note that if the withdrawals taken exceed the growth of the bond, the capital will be eroded.

Unit Trusts and General Investments Accounts (GIAs) pool capital from multiple investors into a single fund, which is then invested across various asset classes, such as stocks, bonds, and property. Investors benefit from an annual dividend allowance of £500 in the 2026/27 tax year, and a capital gains tax annual exemption of £3,000 in the 2026/27 tax year.

Howver, Unit Trusts and GIAs are subject to income tax on any dividends or interests earned, which can reduce the overall tax efficiency of the investment. The tax treatment of these investments can also vary depending on personal circumstances, such as income level and tax bracket.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Under current UK tax law, individuals can give up to £3,000 per year to another person using their annual gifting exemption, including a child or grandchild attending a private school. If you are married or in a civil partnership, you can combine this with your partner’s allowance, resulting in a total annual gifting exemption of up to £6,000 per year.

This offers a tax-efficient way to pay for private school fees. However, financial gifts above £3,000 can be subject to inheritance tax (IHT) if the donor dies within seven years of making the gift. The current nil-rate band for inheritance tax is £325,000 per person.

If a parent has adequate disposable income, this may be utlisied to pay for education costs (including private school fees) under ‘Dispositions for the maintenance of the transferor’s children’ rules.*** A disposition is not a transfer of value for IHT purposes if it is made by one party to a marriage or civil partnership and is both:

– in favour of a child of either party and

– for that child’s maintenance, education or training for a period not ending later than the year ending 5 April in which the child attains the age of 18, or

– after attaining 18, ceases to undergo full-time education

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

***Further criteria applies within the HMRC IHT Manual IHTM04175 which is subject to change.

Many private schools offer means-tested bursaries to help with the cost of tuition. A third of pupils in private education receive means-tested bursaries,3 which can cover up to 100% of fees.

Bursaries are awarded based on financial need, and can be a valuable way for families who may not otherwise be able to afford private school, to access high-quality education for their children. The amount of the bursary awarded is based on a means test, which considers a family’s income, assets, and other relevant factors.

Scholarships are typically awarded based on merit, such as academic or athletic achievement, musical talent, or artistic ability. Scholarships may not cover the full cost of tuition. The proportion of fees covered will depend on the school and the type of scholarship offered.

3 ISC School Fee Assistance, June 2026

Paying private school fees in advance can be a way to save money on the overall cost of tuition. Many private schools offer discounts to parents who pay tuition fees in advance, with the size of the discount increasing with the size of the advance payment.

However, parents considering paying fees in advance should carefully weigh the potential gains against the risks associated with tying up a significant amount of capital in pre-payment.

Depending on the investment chosen, there may be potential for higher returns than the discount offered for advance payment, but there is also a risk of capital loss.